The Hail Mary: How Retail Media Can Weaponize AI Agents to Build a Monopoly

This is part 6 of a series of six articles. Be sure not to miss Part 1 – Retail Media 2.0: Introducing Retail Performance, Part 2 – The Strategic Evolution of E-Commerce, Part 3 – Retail Performance: The Keystone, Part 4 – The Attention Tax, and Part 5 – After the Attention Tax: The Strategic Playbook.

In Parts 4 and 5, I made the case that AI agents will break the Retail Performance Flywheel and proposed a defensive playbook: harvest and hedge. Seven moves to survive the transition.

This article is not about survival.

This article is about the one play that can turn AI agents from an existential threat into a monopoly weapon. It is aggressive, it is expensive, and it will terrify your CFO. It is also, I believe, the single highest-upside strategic option available to any Retail Media platform today.

But — and I cannot emphasize this enough — it only works if it is an entire company strategy. Not a Retail Media initiative. Not a pricing experiment. Not a pilot from the innovation team. A bet that rewires the P&L, the org chart, and the boardroom. Anything less, and you are lighting money on fire.

The Insight: AI Agents Don't Kill the Flywheel. They Supercharge It. For One Winner.

The argument in Part 4 was that AI agents eliminate the attention scarcity that powers Retail Media. That is true for the industry as a whole. But for a single, sufficiently aggressive player, the same dynamic creates something else entirely: the fastest path to monopoly that e-commerce has ever seen.

Here is the logic, and it is disarmingly simple.

AI agents optimize for the user. Their job is to find the best deal — defined as the optimal combination of price, quality, speed, and reliability. They do this across the entire market, in parallel, in milliseconds. They are incorruptible. They are exhaustive. They are perfectly rational.

Now imagine one platform decides to take its Retail Media revenue — the highest-margin business in e-commerce — and reinvest the vast majority of it not into profit but into making its offers objectively, measurably, undeniably superior to every competitor's. Not by a little. By a lot.

Every AI agent on the planet, doing its job honestly, would recommend that platform. Not because the platform bribed the agent. Not because of a commercial deal. But because the agent's mandate is to serve the user, and the platform's offers are genuinely, verifiably the best.

In a world of imperfect human attention, a 15% price advantage might go unnoticed by half your potential customers. In a world of AI agents, a 15% advantage is noticed by every single agent, for every single query, instantly. The return on competitive advantage becomes near-perfect. Every euro you invest in being better translates almost one-to-one into volume — because the information asymmetry that used to protect competitors disappears entirely.

This is the core insight: AI agents don't just create transparency. They create a winner-takes-all accelerant for whoever is willing to be the most aggressive.

The Mechanics: How the Monopoly Flywheel Works

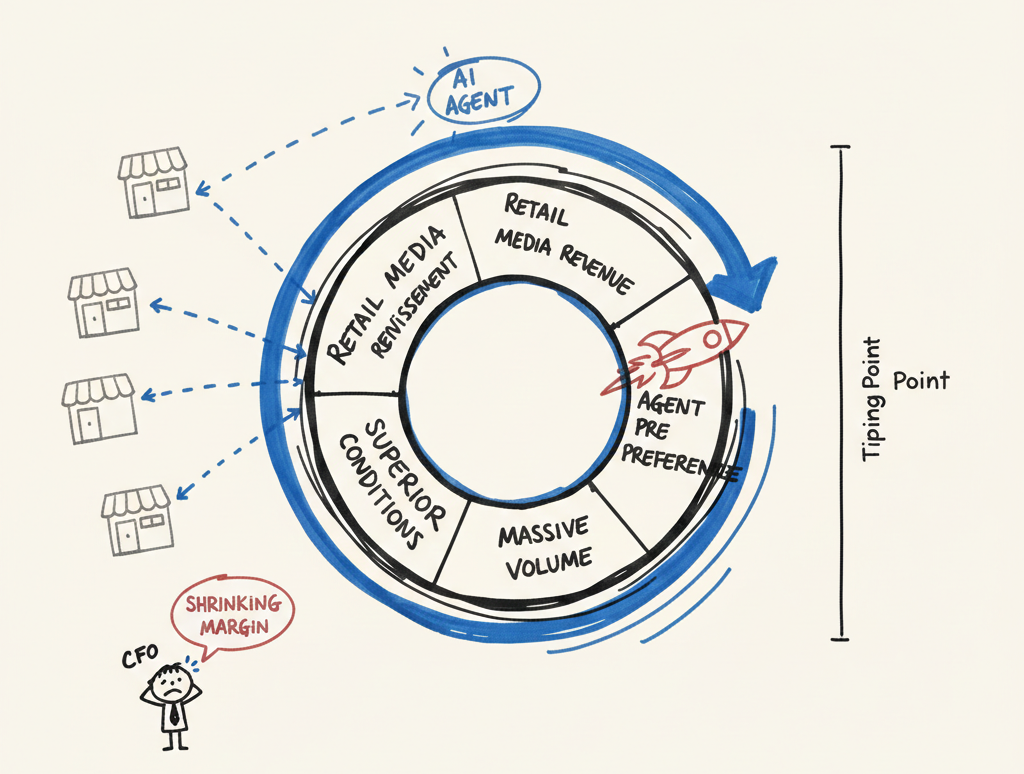

Take the Retail Performance Flywheel from Part 1 and add one modification: instead of extracting Retail Media profit, reinvest it entirely into competitive superiority. The flywheel doesn't break. It accelerates — violently, and in one direction.

Phase 1: The Investment (Year 1–2)

The platform takes 70–80% of its Retail Media revenue and redirects it. Not into shareholder returns. Not into margin. Into making every agent-relevant dimension of the offer objectively superior:

Prices drop 10–15% below market. Delivery speeds accelerate — same-day becomes the default, not the exception. Return windows extend. Service quality jumps. Product data becomes the richest in the market. API response times become the fastest.

Profitability collapses in the short term. The Retail Media team watches its margins evaporate. The CFO sends urgent emails. The board asks uncomfortable questions.

But transaction volume begins to climb. Not linearly — exponentially. Because every AI agent evaluating the market reaches the same conclusion: this platform offers the best deal. And agents don't deliberate. They don't have loyalty to the incumbent. They switch instantly, at scale, without friction.

Phase 2: The Tipping Point (Year 2–3)

Volume reaches a critical mass where a paradox emerges: despite lower margins per transaction, total Retail Media revenue exceeds that of competitors — because the absolute number of transactions is so much higher.

The platform now has both the lowest prices and the highest total advertising income. Competitors face an impossible dilemma: match the prices (and go bankrupt, because their lower volume can't fund the subsidy) or hold their prices (and watch agents route even more traffic away).

This is the tipping point. It is the moment where the flywheel becomes self-sustaining — where the investment in competitive superiority generates enough volume to fund itself. The platform no longer needs to sacrifice margin. The margin comes from scale.

Phase 3: The Monopoly (Year 3–5)

Competitors cannot match the economics. Their Retail Media revenue is shrinking (fewer transactions), their fulfillment costs per unit are rising (less volume over the same fixed infrastructure), and their sellers are migrating to where the transactions are. The death spiral is mechanical and self-reinforcing.

The market consolidates. Not slowly, over a decade, the way Amazon ground down competitors through sheer persistence. Fast. In years rather than decades. Because AI agents don't gradually shift their preferences. They switch categorically, all at once, the moment the data tells them to.

When consolidation is complete, the platform can begin optimizing for margin again. The price subsidies can be partially withdrawn. The Retail Media machine, now operating at monopoly scale, generates returns that dwarf anything the pre-agent era could have produced.

The Elegant Variant: Conditions, Not Just Price

There is a smarter version of this play, and it is the one I would actually recommend.

Pure price dumping has three problems: it attracts regulatory attention, it can be temporarily matched by well-funded competitors, and it trains consumers to expect prices that are unsustainable long-term.

The elegant variant invests Retail Media revenue not primarily into lower prices but into the full spectrum of conditions that agents evaluate:

Fulfillment excellence. Same-day delivery for all products. Two-hour windows in metropolitan areas. Free returns with no time limit. Automated replacement for defective items. These are not discounts — they are structural advantages built on physical infrastructure that takes years to replicate.

Data supremacy. The richest product data on the market. Real-time inventory. Verified seller quality scores. Granular return rate data. Compatibility matrices. Everything an agent needs to make a confident recommendation — available nowhere else.

Risk elimination. Price-match guarantees. Extended warranties funded by Retail Media revenue. Fraud protection. Satisfaction guarantees. Every dimension of purchase risk that an agent can evaluate, reduced to near zero.

Service integration. Post-purchase support that agents can factor into recommendations. Proactive issue resolution. Automatic refunds for delayed deliveries. The kind of service quality that makes an agent's job easy — because recommending this platform means recommending the lowest-risk option.

The beauty of this approach: agents don't just evaluate price. They evaluate the entire offer. A platform that is 5% more expensive but delivers in half the time, has a 3% return rate versus 25%, and offers instant refunds for any issue — that platform wins the agent's recommendation on the total value proposition. Every time.

And this advantage is radically harder to copy than a price cut. A competitor can match your prices by burning cash. They cannot match your logistics network by burning cash — not in a quarter, not in a year. They cannot replicate your proprietary data by raising a funding round. They cannot build your seller quality infrastructure with a board presentation.

The conditions-based variant reaches the same monopoly tipping point, but through advantages that are structural rather than financial. That makes them more sustainable, more defensible, and less regulatorily exposed.

Why This Cannot Be a Department Strategy

Now the part that most companies will get wrong.

The play I just described requires the simultaneous, coordinated transformation of:

Retail Media. Must accept that its margins will be temporarily destroyed in service of a company-wide strategy. The highest-margin department in the company must become the funding engine for everyone else. This is not a "Retail Media pivot." It is a Retail Media sacrifice — one that only makes sense if every other department executes in lockstep.

Pricing. Must implement dynamic pricing that is not optimized for margin but for agent preference. This is the opposite of what every pricing team has been trained to do. The KPI changes from "gross margin per unit" to "agent recommendation rate." That is a fundamental reorientation, not a parameter tweak.

Fulfillment and logistics. Must absorb massive investment — funded by Retail Media revenue — to build delivery speed, reliability, and return infrastructure that becomes the primary competitive moat. Fulfillment transitions from cost center to the most strategically important function in the company.

Product data and technology. Must build the agent-grade API infrastructure described in Part 5, with tiered data access, sub-50ms response times, and structured merchandising feeds. This is not an IT project. It is the new storefront.

Seller relations. Must manage the seller base through a transition where Retail Media becomes Agent Media — where sellers invest not in visual placements but in data enrichment, conditional advantages, and outcome-based programs. Sellers will resist. The commercial team must bring them along.

Finance. Must model a 2–3 year period of depressed margins and present it to the board not as a problem but as an investment thesis with a defined payback horizon. This requires a CFO who understands strategic investment, not just cost management.

The CEO and the board. Must own the strategy. Must defend it against quarterly pressure. Must accept that the company will look worse on paper for several years before it looks dramatically better. Must have the conviction to stay the course when competitors whisper that the strategy is failing.

If any one of these functions opts out, the strategy collapses. If Retail Media protects its margins, there is no subsidy to invest. If fulfillment doesn't absorb the investment, there is no moat. If pricing optimizes for margin instead of agent preference, the volume advantage never materializes. If technology doesn't build the API, agents can't even find the superior offers. If the board loses nerve after three quarters of declining margins, the investment is wasted.

This is why the play is a Hail Mary. Not because the logic is wrong — the logic is some of the soundest strategic reasoning available in e-commerce today. But because executing it requires an entire organization to row in one direction, for years, against every short-term incentive.

There is no version of this strategy that works as a Retail Media department initiative. There is no version that works as a "pilot." There is no version that works with half-commitment. It is all or nothing, and "all" means every function, every budget line, every KPI, and every board meeting aligned to a single thesis: we will be the platform that every AI agent recommends, whatever it takes.

The Historical Parallel

This is not unprecedented. Amazon executed essentially this strategy in the 2010s — sacrificing margins systematically to build scale, infrastructure, and market dominance, funded by the high-margin businesses (AWS initially, then Retail Media) that subsidized below-market pricing and above-market fulfillment.

The difference is speed. Amazon executed over a decade, in a world of imperfect human price comparison. The AI agent-accelerated version compresses this timeline to 3–5 years — because agents eliminate the information friction that slowed Amazon's original flywheel. When every consumer has a perfect price-comparison machine working for them 24/7, competitive advantages translate into market share gains almost instantaneously.

The second difference is risk. Amazon operated in an era of lighter regulatory scrutiny for platform businesses. Today's environment — the EU Digital Markets Act, national competition authorities, political attention on tech concentration — means the monopoly path is more regulated. The conditions-based variant I described is specifically designed for this reality: it builds dominance through service superiority rather than price predation, making it far harder to attack on competition law grounds.

The Honest Assessment

I want to be direct about who should and should not consider this play.

This strategy is viable for: A platform that is already a top-3 player in its market, has significant Retail Media revenue to redirect, possesses meaningful fulfillment infrastructure to build on, has a board and leadership team capable of multi-year conviction, and operates in a market large enough to reward monopoly-scale economics.

This strategy is not viable for: Mid-sized platforms without the capital reserves to absorb 2–3 years of margin compression. Companies with fragmented governance where department heads protect their own P&Ls. Platforms that are primarily marketplaces without owned fulfillment. Organizations where the board evaluates management on quarterly EBITDA.

This strategy will fail if: It is treated as a Retail Media optimization. It is piloted in one category. It is attempted without board-level commitment. The CFO is not a co-architect. Fulfillment investment is deferred. The pricing team retains margin targets.

Conclusion: The Fork in the Road

Every Retail Media platform now faces a fork.

The safe path — harvest and hedge, as described in Part 5 — preserves optionality and manages the transition gradually. It is the right choice for most companies. It is prudent, defensible, and executable.

The aggressive path — the Hail Mary described in this article — is the play that produces a monopoly. It takes the same AI agent dynamics that threaten the industry and turns them into the most powerful concentration mechanism in the history of e-commerce. It is the play that creates the next Amazon-scale outcome.

But it requires something that almost no company possesses: the willingness to make a bet that touches every function, suppresses short-term profit, and demands years of coordinated execution against every instinct of conventional management.

It requires, in other words, a real strategy. Not a Retail Media strategy. Not a pricing strategy. Not a technology strategy. A company strategy — singular, total, and irrevocable.

The platforms with the courage to attempt it, and the organizational discipline to execute it, will not just survive the AI agent era.

They will own it.

Key Takeaways

- The Monopoly Mechanism: AI agents create perfect price and quality transparency. A platform that makes its offers objectively superior across all agent-evaluated dimensions will be recommended by every agent — creating a faster path to monopoly than any previous era of e-commerce allowed.

- The Elegant Variant: Invest Retail Media revenue not just into lower prices but into fulfillment speed, data richness, service quality, and risk elimination — conditions that agents evaluate, competitors cannot quickly replicate, and regulators cannot easily classify as predatory pricing.

- The Tipping Point: When volume reaches a level where total Retail Media revenue exceeds competitors' despite lower per-transaction margins, the flywheel becomes self-sustaining and competitors enter a structural death spiral.

- The Organizational Requirement: This is not a Retail Media initiative. It requires simultaneous transformation of pricing, fulfillment, technology, seller relations, and finance — all directed by CEO and board commitment over a multi-year horizon.

- The Honest Filter: Viable only for top-3 market players with significant Retail Media revenue, owned fulfillment infrastructure, capital reserves for margin compression, and governance structures that support multi-year strategic bets.

Frequently Asked Questions

Can Retail Media revenue really fund a monopoly strategy?

Yes, because Retail Media is the highest-margin business in e-commerce. The margins typically range from 50–80%, compared to 3–5% on core commerce. Redirecting 70–80% of this revenue into competitive superiority — lower prices, faster fulfillment, richer data — while accepting short-term margin collapse, can create volume advantages that become self-funding within 2–3 years.

Why do AI agents accelerate monopoly formation?

In a human-mediated market, competitive advantages are partially invisible — consumers don't compare exhaustively. AI agents compare everything, instantly, across all competitors. This means every incremental improvement in price, speed, or service translates almost directly into volume gains. The return on competitive investment approaches 1:1, which is unprecedented in e-commerce history.

Why can't this strategy work as a Retail Media department initiative?

Because it requires sacrificing Retail Media margins (the department's core KPI) while simultaneously demanding massive investment from fulfillment, technology, pricing, and seller relations. No department will voluntarily destroy its own metrics to fund another department's transformation. Only a CEO-led, board-backed company strategy can align these competing interests.

What is the difference between the price-based and conditions-based variant?

The price-based variant simply undercuts competitors on price, funded by Retail Media revenue. It is fast but regulatorily risky (potential predatory pricing classification) and easy to temporarily match. The conditions-based variant invests in fulfillment, data quality, service, and risk elimination — advantages that agents evaluate alongside price, that are structurally harder to replicate, and that are far less exposed to competition law challenges.

How does this strategy relate to Amazon's historical approach?

Amazon executed a similar logic in the 2010s: sacrificing margins to build scale and infrastructure, subsidized by high-margin businesses (AWS, later Retail Media). The AI agent-accelerated version compresses this from a decade to 3–5 years, because agents eliminate the information friction that slowed the original flywheel. However, today's stricter regulatory environment requires the conditions-based variant rather than pure price predation.

This concludes the extended series on Retail Media and Retail Performance. Parts 1–3 built the framework. Parts 4–5 challenged and extended it. Part 6 placed the bet. The question is: will you?